Management accounting presented inunderstandablehumanaccessiblelanguage.

Management accounting presented inhumanaccessiblelanguage.

Defines how many times during the reporting period the inventory goods are transformed into the goods sold.

The higher the figure, the faster the finished products at the warehouse are turned into the goods sold and the less money is frozen in a warehouse in the form of stocks. The lower the figure, the more money is frozen in stock.

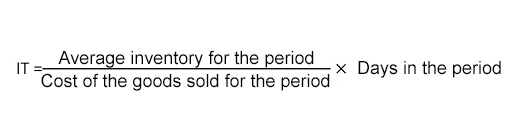

It is calculated by formula:

Average inventory for the period is determined similarly to the average value of shareholders’ equity (see ROE).

The second possible variant is calculated in days.

In this case inventory turnover (IT) shows how many days have passed since the date of new goods arrival at the warehouse till the date of shipment.

It is calculated by formula:

Where can we get the figures?

Cost of the goods sold for the period can be found in the line 2, Profit and loss account.

Inventory can be found in the line 2.2, Section 2 “Current assets”, Balance sheet.