Management accounting presented inunderstandablehumanaccessiblelanguage.

Management accounting presented inhumanaccessiblelanguage.

Well, your accountant is presenting balance sheet, profit and loss account as well as cash flow statement prepared for the previous month. Even if you trust your employee and find him/her reliable, you should be able to make the express check anyway.

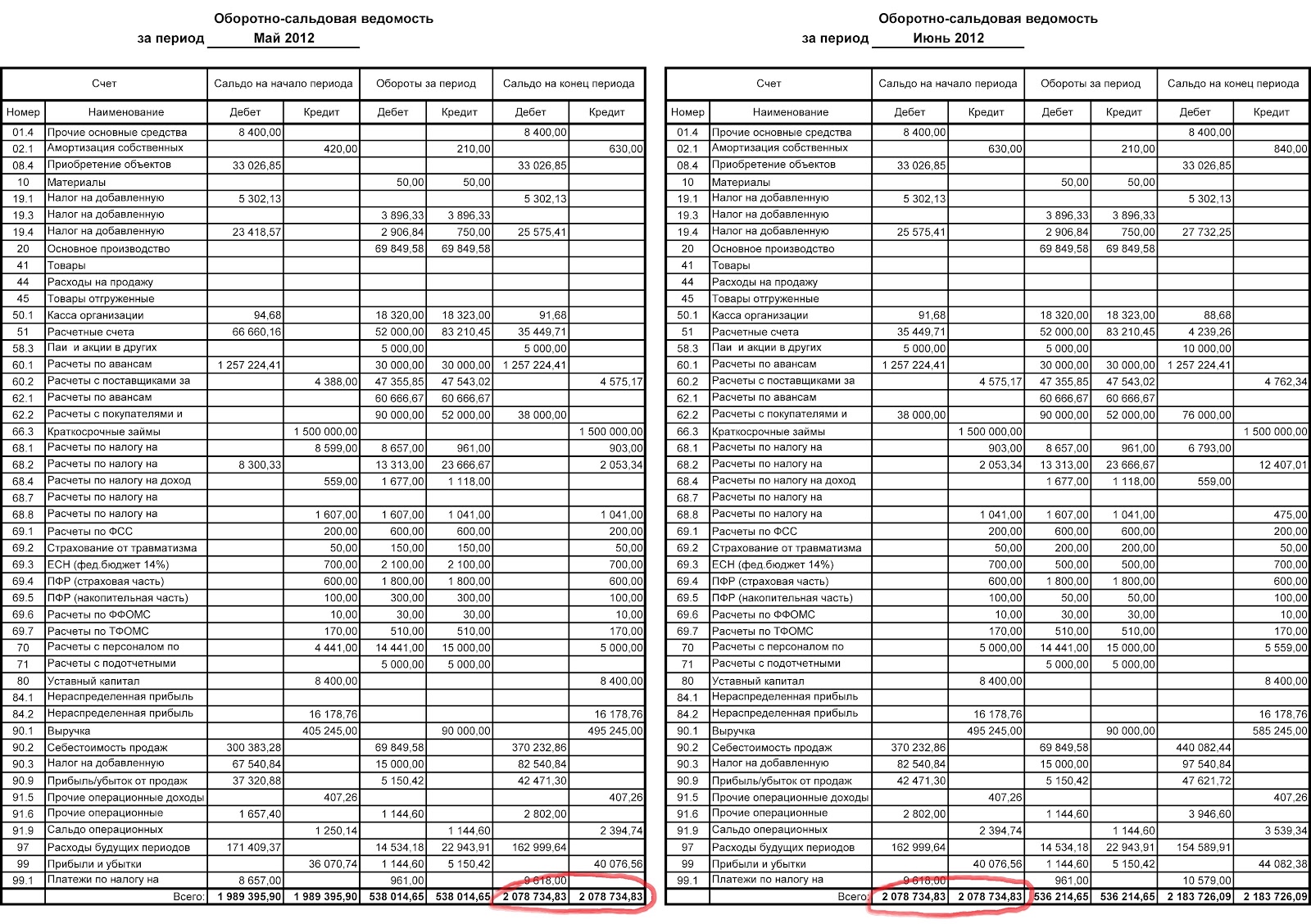

THESE FIGURES ARE TO BE ABSOLUTELY IDENTICAL TO EACH OTHER, UP TO THE LAST PENNY!!!

Your turnover is not important here, neither your schemes of distribution and cash flows, nor the sum of money your company is working with. Closing balance figures

at the end of the previous accounting period are to be equal to the opening balance figures at the beginning of the current accounting period. If these figures differ, the accountant should provide the reasons and explanations how it has happened. It is a crucial moment which allows you to realize the absence of changes in the previous accounting periods.

Turnover balance sheet is an integral part of all the statements and the verification stated above is to involve the documents from different statements. For example, when you make the statement for the month of June you should compare the turnover balance sheets for the months of June and May.

Under Clauses 2 and 3 you will see just the right order of these forms construction, no more.

If you need more thorough check, you should inspect the main clauses of the balance sheet:

To verify the correctness of this clause you need to study the inventory of fixed assets. As a rule, this procedure is used no more than once a year.

To check if the inventory storage balances are in compliance with the documents, you need to study the inventory stock-taking. The procedure of stock-taking is to be

used at least once in three months, but some activities (such as sale of oil products) require a check on a monthly basis. A full inventory is time-consuming in case of very large balances and large warehouse product mix, thus, partial inventory is taken by separate items.

To confirm the correctness of the data in accounts receivable and accounts payable the accountant should provide reconciliation statements between your company and each of your debtors. As a rule, it is useless to check all the contractors, it is enough to check the basic ones connected with the main trade turnover and money circulation.

Cash assets of the enterprise are stored on the settlement account and in the cash office. So, in order to check the correctness of the information in the balance sheet, you should compare the settlement accounting data with the information from the “Client-Bank” programme, and cash office accounting data with the cash book accordingly.

If you want to check the correctness of the information about the petty cash in the hands of employees, you need to ask all the employees to close their subreports on a given date (within 2-3 day, at most). There are two ways to close the subreports:

Thus, in 2-3 days (no more!) after the order mentioned above:

After checking you can distribute the funds among the employees who need them.